Measurement and metrics for ESG issues are becoming increasingly important in decision-making by investors, regulators, business partners, and consumers. But what are ESG metrics, really? What do they look like and why are they important?

What is an ESG metric?

In general, a metric is a quantitative or qualitative measure used to track progress and evaluate success. For businesses, metrics are used to track progress and performance in certain areas that are critical to the viability and performance of a business, such as revenue, profitability, customers, employees, etc.

When we talk about ESG metrics, we’re really talking about performance measures or indicators of a company’s performance on environmental (E), social (S), and governance (G) issues. They are similar to other business metrics in that they're used to assess a company’s operating performance and risk. These metrics can come from standards, frameworks, or regulations that ask for very specific information. Or, they can simply stem from a company's KPIs that are associated with ESG, even if they’re not linked to any specific standard or framework. While ESG metrics (performance measures) can be either quantitative or qualitative in nature, companies will still need to provide very specific information on distinct topics. Examples of ESG metrics include indicators like greenhouse gas (GHG) emissions intensity, waste production levels, and board gender diversity.

Conventionally, investors use financial data and metrics to determine the feasibility of investing in a company. Nowadays, they have been turning to ESG metrics to assess the viability and long-term performance of companies based on non-financial ESG risks and opportunities alongside traditional business metrics.

What’s an ESG standard, framework, or questionnaire? And, how do they differ?

The ESG landscape encompasses distinct tools—ESG standards, frameworks, regulations, and questionnaires. Each contributes differently to sustainability reporting and management. More specifically:

•Standards offer detailed disclosure criteria including specific performance measures or metrics, focusing on public interest and requiring rigorous governance.

•Frameworks provide a high-level context and guiding information without specifying metrics. Frameworks prescribe high-level disclosures and are followed alongside standards.

•Regulations encompass a set of rules or guidelines mandated by regulatory authorities to govern ESG practices. They wield significant influence over market dynamics, being inherently mandatory and shaping fundamental changes (e.g., the Corporate Sustainability Reporting Directive).

•Questionnaires, administered by third parties, aim to assess sustainability performance through an ESG rating or score, with voluntary participation from companies. However, their methodology tends to be less accessible to the public and less transparent compared to standards or frameworks...

Despite these distinctions, the space is somewhat unclear at the moment, as each standard and framework possesses its own set of topics and performance measures, which can either vary significantly or overlap.

While the landscape is evolving rapidly, the overall trend points toward the convergence of performance measures and the establishment of common ESG metrics, signaling a need for ongoing efforts—especially in the area of climate change. As such, the direction of travel is pointing to:

- An alignment of general disclosures with the TCFD Recommendations' four pillars;

- Increased focus on universal topics like diversity and climate change, with associated performance indicators;

- Industry-specific topics and metrics are being identified as material, requiring companies to justify their determination of materiality or explain why certain topics are not addressed.

Quantitative vs. qualitative ESG metrics

The nature and variability of many ESG metrics is one of the main challenges that companies face today. Unlike financial datasets that are mostly numerical, ESG metrics can include both quantitative and qualitative data to help investors and other stakeholders understand a company’s actions and intentions.

Quantitative metrics are numerical values that can be easily computed and compared over time or between companies. They convey information about quantities, distances, percentages, and so on. Unlike financial metrics, they come in many different measurement units, not just dollars.

Qualitative metrics are usually more challenging to collect, calculate, and compare than their quantitative counterparts. But, because they describe qualities, characteristics, strategies, processes, and actions that cannot be numerically measured, they’re also highly useful to both complement and contextualize the disclosure of quantitative data.

One example of a qualitative metric would be a description of a safety management system, including its implementation, testing procedures, and the resulting outcomes. The “S” pillar of ESG frequently falls into the qualitative camp, such as Diversity, Equity, and Inclusion (DEI) initiatives or a company’s impacts on the communities in which it operates.

When it comes to reporting on their ESG issues, companies typically use both quantitative and qualitative metrics. In turn, this helps them provide a more holistic view of their sustainability performance to stakeholders.

What types of topics do ESG metrics cover?

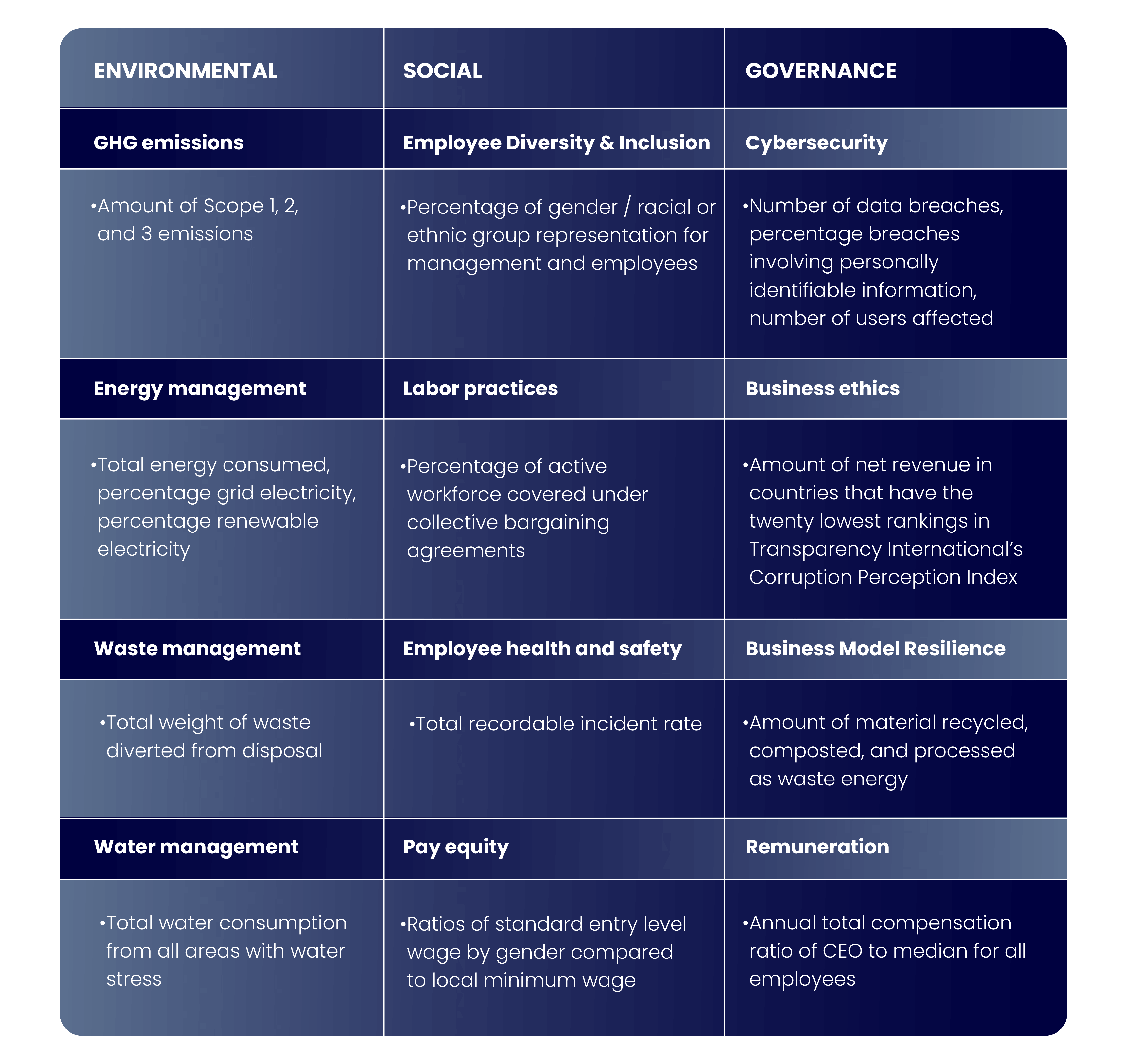

Due to the various ways in which a business can influence and be influenced by the environment and society, ESG issues encompass a vast array of data points. ESG metrics are categorized into different topics or pillars, each branching into specific individual metrics.

Here are some ESG metrics examples (specific ESG topics and their respective performance metrics):

How do you know which ESG metrics to use?

- Start by identifying your material ESG issues. i.e., those that matter to your operating and financial performance, or that matter to the protection of the environment or the betterment of society.

- Review whether your company is in scope for any ESG regulation in its operating region(s). For example, the CSRD for companies that do business in the EU, or the U.S. Securities and Exchange Commission (SEC) Climate Disclosure Rule for publicly listed firms in the United States.

- Refer to the main standards or frameworks that offer specific performance measures or metrics on these topics—for instance, the ones that are prescribed by the regulations—and identify the ones that make sense to you. These may include metrics that you may already be measuring, or those that can help you better manage the specific material issues your company has already identified.

Examples of standards or frameworks offering specific ESG performance measures or metrics

Global Reporting Institute (GRI) - disclosure standards

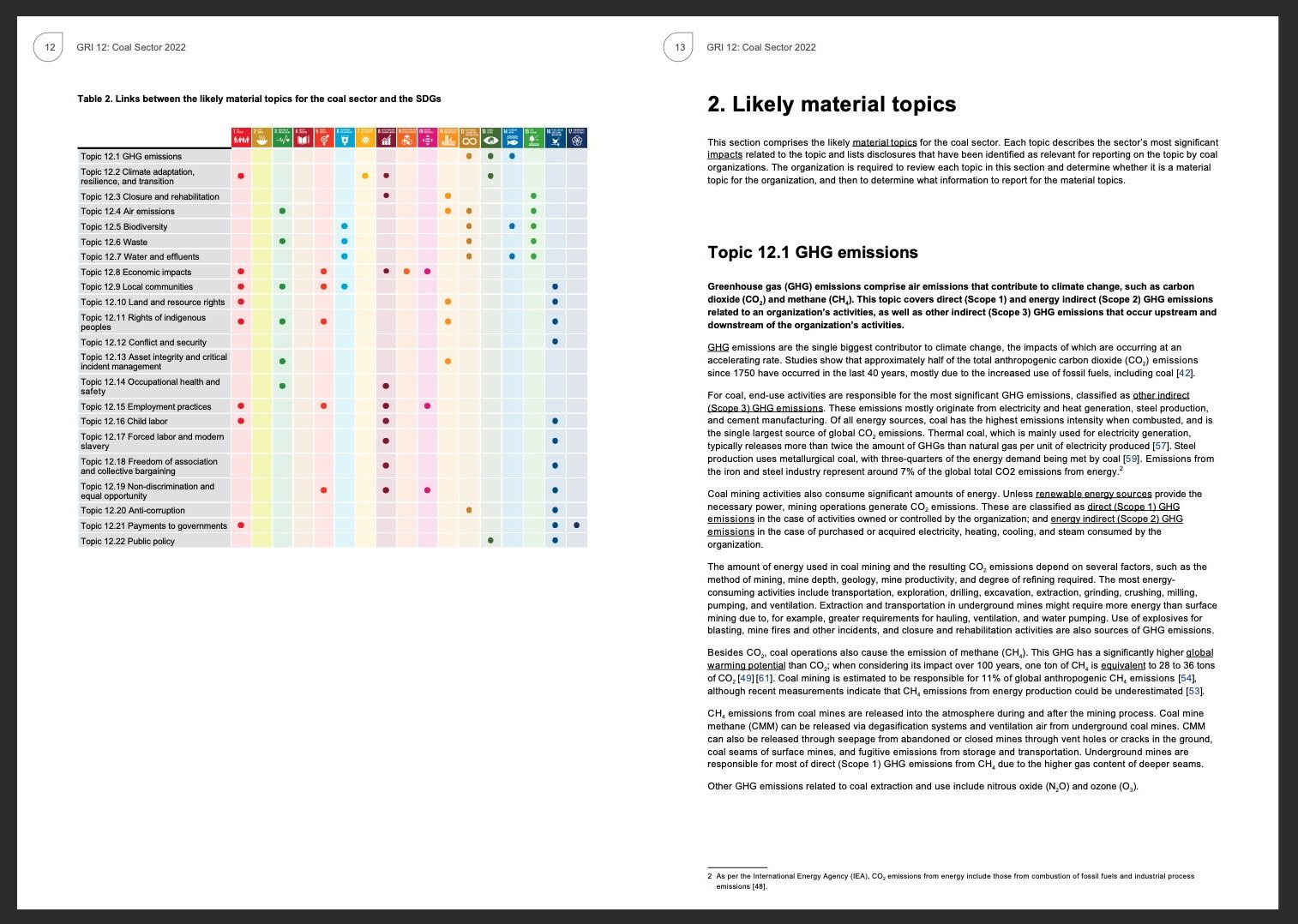

The GRI is an independent, international, and non-governmental organization providing sustainability reporting standards (GRI Standards) to enable consistent communication surrounding their impacts on sustainable development, both positive and negative. Released in 2010, these standards categorize metrics into Universal (for all companies), Sector (industry-specific), and Topic (material impacts) Standards. In October 2021, the GRI updated its Universal Standard and introduced the first Sector Standard for Oil and Gas, announcing plans for additional sector-specific standards such as the recently published GRI 101: Biodiversity 2024 standard.

Here is an example of the GRI Coal sector standard:

To download the GRI universal, sector, and topic standards click here. Start by identifying the topics that are material to your business, then choose the standard that best corresponds to each of these topics.

Here is an example of GRI ESG Standards document:

Moreover, the GRI has entered into collaborative agreements with the European Financial Reporting Advisory Group (EFRAG) to develop the European Sustainability Reporting Standards (ESRS), and with the International Sustainability Standards Board (ISSB) to draft the IFRS Sustainability Disclosure Standards.

For a more comprehensive overview of the GRI, explore our blog post “The Global Reporting Initiative—what is it and how can GRI reporting software help?”

Sustainability Accounting Standards Board (SASB) - disclosure standards

SASB is an independent, not-for-profit organization established in 2011 to set standards for companies to disclose sustainability or ESG information to investors and other providers of financial capital. SASB identifies industry-specific performance measures or metrics for 77 industries. While different industries may have the same material topic, they may have different performance measures on this topic based on the nature of their activities.

To download the publicly available standards and see their underlying ESG metrics, click here. First, locate your industry, and then download the corresponding SASB standards.

In 2021, SASB and IIRC merged to form the Value Reporting Foundation (VRF). By August 2022, the VRF integrated into the IFRS Foundation under the ISSB, establishing a comprehensive set of global corporate sustainability disclosure standards. The ISSB aims to utilize SASB's industry-specific standards and its standard-setting process in crafting its standards.

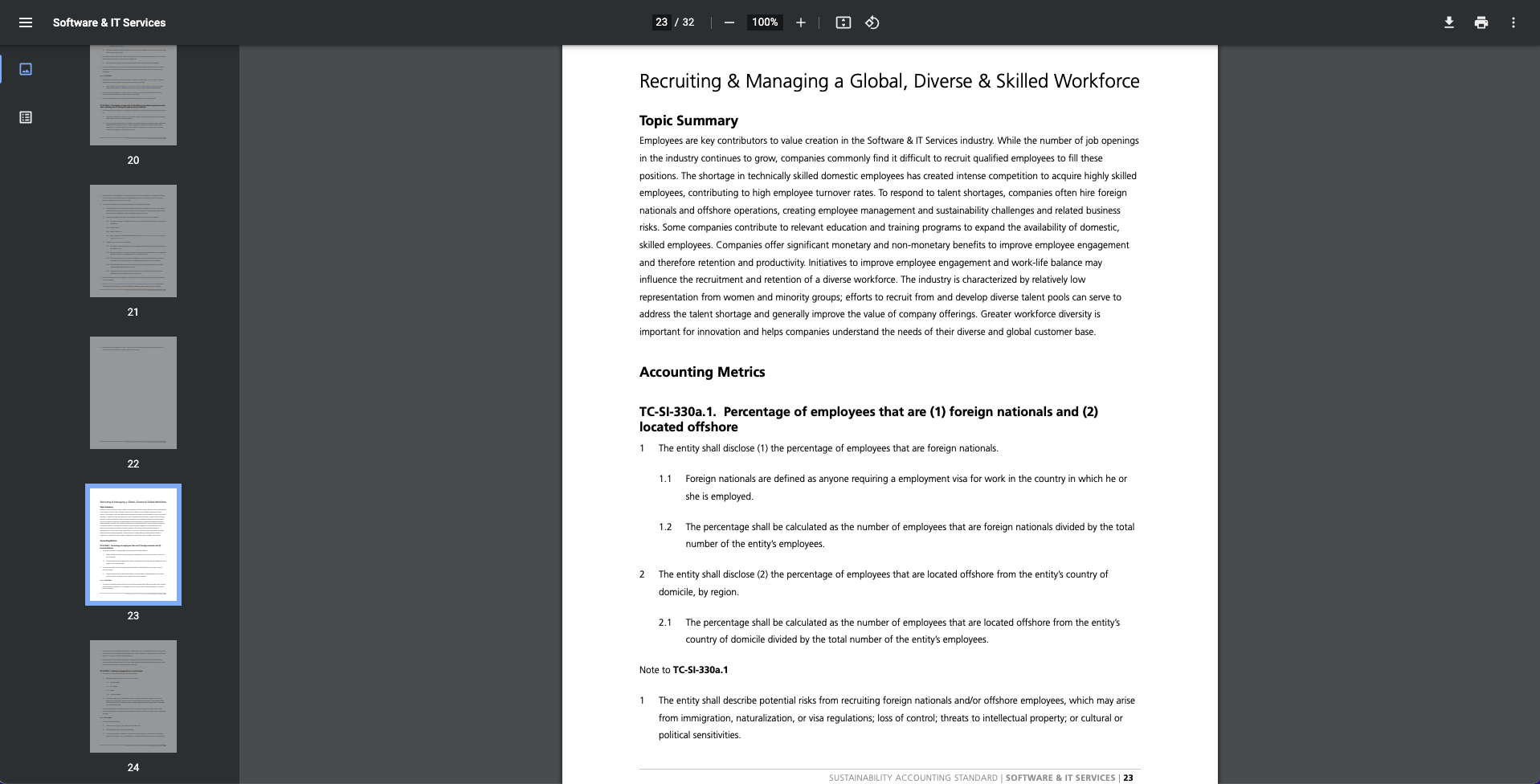

Here is an example of SASB ESG Standards document:

Corporate Sustainability Reporting Directive (CSRD)

The CSRD is an EU regulatory directive designed to enhance corporate sustainability disclosures. In line with CSRD, the European Commission has also approved the European Sustainability Reporting Standards (ESRS) delegated act, which sets out a comprehensive set of standards for the disclosure of environmental, social, and governance information.

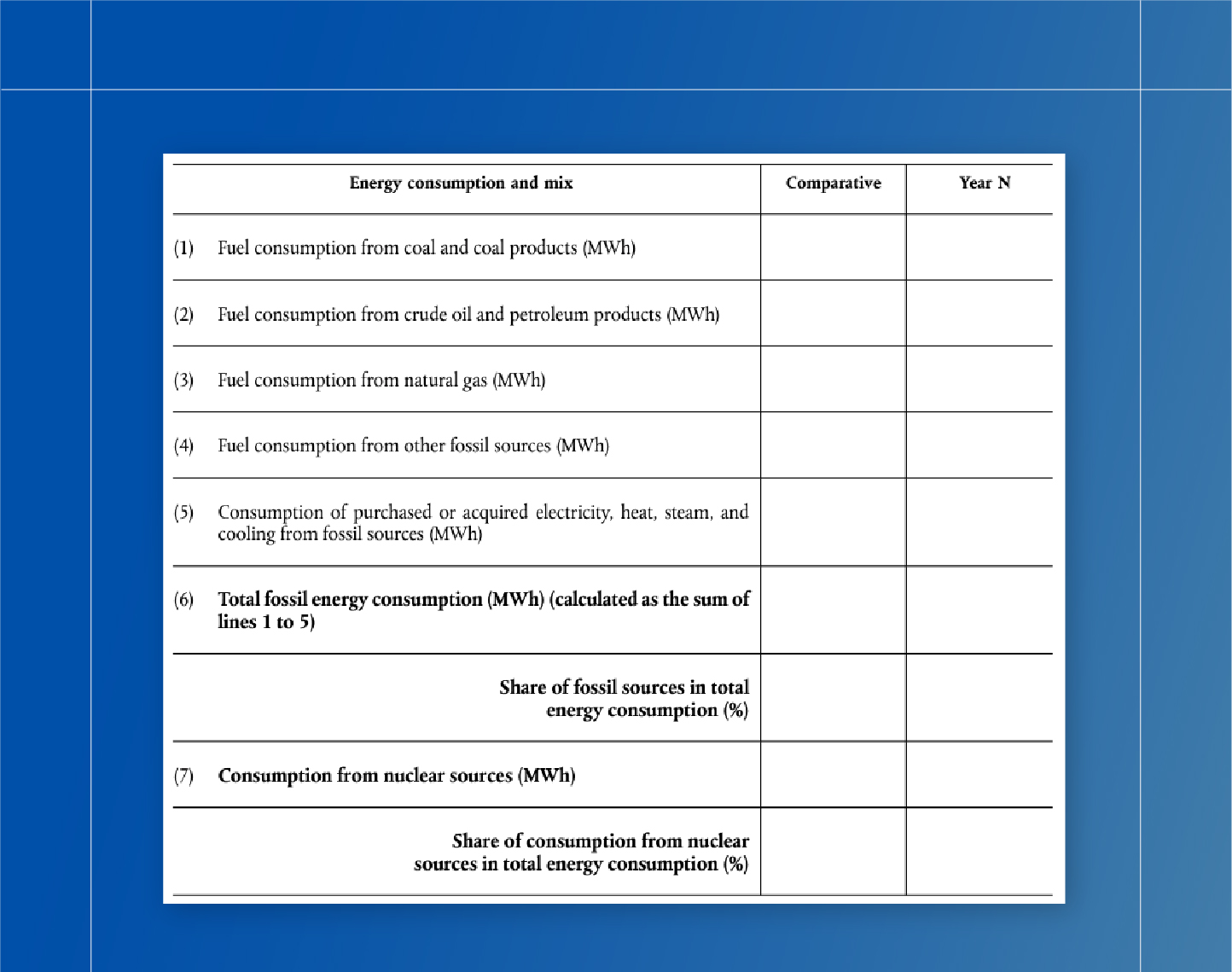

The ESRS standards encompass cross-cutting standards (general requirements and general disclosures), and topical standards regarding the environmental, social, and governance spheres. Here is an example of the ESRS standard for climate change, along with the key metrics requested for energy consumption:

Why is ESG management software important for managing ESG metrics?

The complexity of ESG metrics, along with the multiple frameworks, standards, and questionnaires in existence, makes it difficult for companies to compile, organize, and report on their performance using ESG metrics that are relevant to them. And, because they commonly struggle with complex data-gathering processes, poor data quality and a lack of appropriate assurance, they’re also forgoing—albeit, inadvertently—the value-creating potential of better managing their material risks and opportunities.

As the focus on sustainability and ESG issues continues to rise, so will the need for more (and higher-quality) ESG information, including the need for reliable and comparable quantitative and qualitative ESG metrics. But, for ESG data to be available, comparable, and reliable, it needs to be regulated, standardized, and externally assured. And, to meet all of these requirements efficiently, ESG data and ESG performance metrics must first be digitized.

Novisto’s ESG management platform is designed to digitally transform ESG program management. We ensure that corporate ESG data, workflows, and reporting are trusted (read: auditable, like financial data), efficient (automated and streamlined), and insightful (contextualized, with clear guidance for decision-making). Novisto also integrates major standards, frameworks, and questionnaires to facilitate companies’ data collection and reporting practices.

To see us in action, book a demo today.