In the dynamic corporate sustainability landscape, the Corporate Sustainability Reporting Directive (CSRD) emerges not only as a monumental leap in terms of scope, complexity, and reporting requirements but also as an indicator of the future trajectory of corporate sustainability disclosures.

More than anything, the CSRD embodies a paradigm shift in how companies will be required to approach their sustainability reporting. Namely: what was once a voluntary exercise is now becoming a mandatory, structured, and externally assured business practice, on par with traditional financial reporting.

What is the CSRD?

Effective as of January 1, 2024, the CSRD is an EU regulatory directive created to strengthen sustainability disclosure and accounting rule-making, fostering greater transparency and long-termism. It amends and builds upon its predecessor, the Non-Financial Reporting Directive (NFRD), which initially focused on the largest publicly listed companies in Europe. While this represents a sizeable step up from the NFRD, it’s ultimately an evolution from an existing framework (rather than a completely new initiative).

Under the CSRD, companies must report using the European Sustainability Reporting Standards (ESRS), developed by the European Financial Reporting Advisory Group (EFRAG). The ESRS aim to streamline relevant pieces of EU legislation such as the EU Taxonomy Regulation and the Sustainable Finance Disclosure Regulation, while taking into account the work of global standard-setting initiatives for sustainability reporting.

Furthermore, the CSRD requires transposition into national laws, a process expected to unfold over the coming year.

Double materiality is foundational

To report under the ESRS, companies will need to disclose sustainability information based on the “double materiality” principle. Essentially, this will require companies to conduct a due diligence assessment to determine their material dependencies and impacts on the environment and people (i.e., impact materiality), as well as the material risks and opportunities to their operations and financial performance (i.e., financial materiality).

For guidance on how to approach the CSRD’s double materiality principle, explore our white paper: Seizing the CSRD Opportunity.

Key impacts of the directive

The CSRD is anticipated to have far-ranging impacts, including increasing the comparability of sustainability information. More specifically, we expect it to have a significant impact in the following areas:

- Reduced cost of sustainability reporting: The CSRD is expected to clarify and provide certainty about the sustainability information that needs to be reported, making it easier to obtain information from business partners such as suppliers, clients, or investee companies. Moreover, it’s expected to lessen the number of requests companies get for sustainability information.

- Reduced systematic risks to the economy: More complete disclosures are expected to improve the targeting of financial capital toward companies and initiatives that address social, health, and environmental issues.

- Global coverage and harmonization of sustainability reporting standards: The ESRS were developed by leveraging and incorporating existing standards and frameworks, such as the Task Force on Climate-related Financial Disclosures (TCFD) and the Global Reporting Initiative (GRI). More than a major milestone in the EU, this also supports reporting harmonization efforts on a global scale.

Who is in scope?

All large companies and all publicly listed companies—with the exception of microenterprises—are in scope. This means that ~50,000 EU companies will have to report sustainability information compared to the ~11,600 under the NFRD. However, publicly listed small and medium enterprises (SMEs) will be exempted from the CSRD until 2028. For additional details on the size and scope of applicable companies, please refer to the CSRD Fact Sheet.

So, how is the CSRD pushing the envelope?

The CSRD paradigm shift is not merely a matter of compliance or box-ticking: it represents a fundamental recalibration of corporate priorities and practices, catalyzed by double materiality assessments. The European Union, by setting exceptionally high standards, has raised the bar for sustainability reporting worldwide.

Moreover, this isn’t occurring in isolation. The CSRD—alongside the U.S. SEC climate-related disclosure rule, and SB 261 & SB 253 on climate-related disclosures in California—all epitomize the evolution that’s underway.

What does this new direction signal?

Heightened interoperability: Convergence with other standards and frameworks

The CSRD is part of wider global efforts to enhance convergence in sustainability reporting, delivering much-needed uniformity—and potentially, a global baseline—to a fragmented ESG disclosure landscape. Thus, to increase the comparability of sustainability information between companies, the ESRS were designed to increase interoperability with existing standards and frameworks. For instance, EFRAG engaged in regular technical dialogue with the International Sustainability Standards Board (ISSB) during the drafting of the IFRS Sustainability Disclosure Standards (SDS).

Moreover, EFRAG and the GRI have jointly claimed to exhibit a high degree of interoperability. In November 2023, they signed a new MoU to substantiate the benefits of the alignment between the two sets of standards, and to continue working together to deliver technical support for reporting companies. Their collaboration also includes fostering interoperability of digital XBRL taxonomies, with a simplified tagging system and digital correspondence table between both standards.

Ultimately, heightened interoperability between the ESRS and other standards will greatly ease the reporting burden for many companies, eliminating the need to report the same sustainability information twice (or thrice) through separate, overlapping standards.

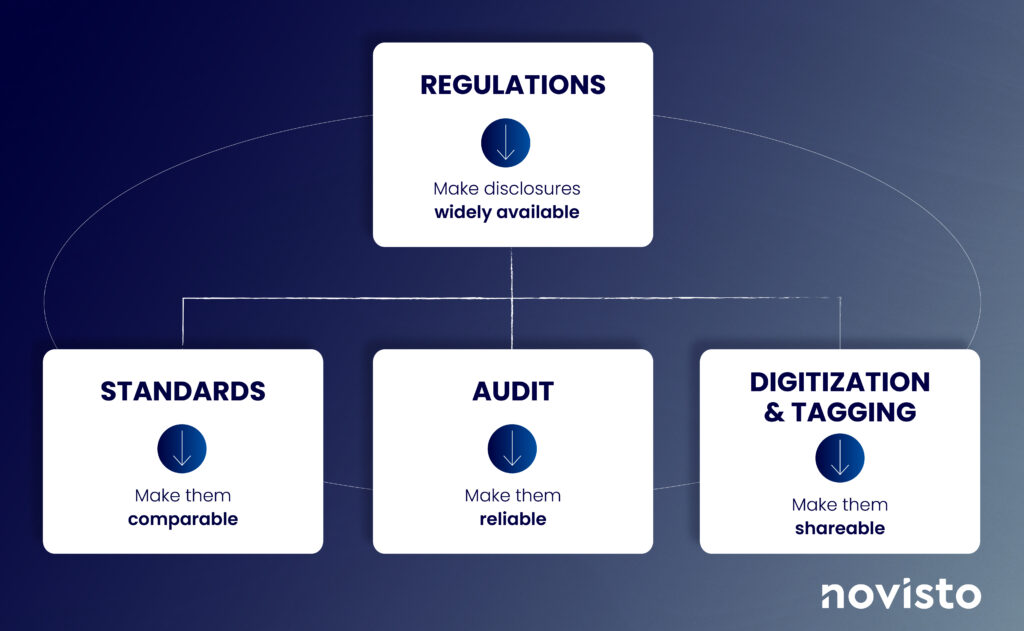

Disclosures must be: Comparable, reliable, and shareable…

The lack of quality and consistency in sustainability information under the NFRD, coupled with mounting climate risks, has driven the need for more widely available and reliable corporate disclosures.

The CSRD regulation aims to address this by mandating that companies standardize, audit, and digitize their sustainability reporting. This push for enhanced transparency will empower stakeholders to make more informed decisions, driving meaningful progress on sustainability.

The CSRD is making disclosures comparable

The CSRD will make disclosures standardized via the application of the ESRS standards, mandatory for all in-scope companies. Thus, through the ESRS, the CSRD is fostering greater comparability.

The CSRD is making disclosures reliable

The CSRD will make disclosures reliable by requiring them to be audited. Therefore, producing externally assured disclosures is mandatory for all in-scope companies, starting with limited assurance in the first year and extending to reasonable assurance over time.

The CSRD is making disclosures shareable

The CSRD will make disclosures widely shareable and discoverable by requiring companies to produce a digital and XBRL-tagged report, making them both human- and machine-readable.

EFRAG has launched a public consultation on the draft XBRL Taxonomy for the first set of ESRS (ESRS Set 1). This taxonomy enables the digital tagging of ‘ESRS statements’ (aka ‘disclosures’) by providing XBRL elements (or ‘tags’) for every data point and dimensional disaggregation defined in the ESRS disclosure requirements. The ESRS XBRL taxonomy is expected to be introduced and finalized in 2024.

Convergence with financial reporting

The CSRD exhibits strong convergence with financial reporting. For one, sustainability information will need to be included in the management report and not in a separate sustainability report. This will place sustainability disclosures in regulatory filings for the same reporting period as financial information.

Challenges & opportunities ahead

While undeniably beneficial for stakeholders and the planet, the comprehensiveness and unprecedented depth of the CSRD have raised concerns. For one, the level of granularity and prescriptiveness it demands is unparalleled—in total, the ESRS encompasses 1,144 data points, a mixture of both quantitative and qualitative information.

Furthermore, the cornerstone of the CSRD—the double materiality principle—will profoundly shape the type of sustainability information companies collect and how they collect it. But tackling a double materiality assessment (DMA) is no easy feat, and the risk of missteps is significantly high. That said, companies will need to approach their DMAs with the right mindset and proper guidance.

Challenges notwithstanding, the CSRD will also create new opportunities for companies to embed sustainability into their business models.

CSRD software for global enterprises

The CSRD signals a clear direction of travel, epitomizing how corporate sustainability reporting is changing. Whether or not your company is subject to the CSRD, the directive has cast a long shadow, raising the bar on data rigour, quality, and relevance.

Starting in 2024, companies subject to the existing NFRD will need to make their disclosures comparable, reliable, and shareable. Luckily, there are software providers, like Novisto, that exist to address these requirements.

Our all-in-one CSRD software is helping global companies seize the opportunities brought on by this new directive. From simplified data collection and approval workflows to investor-grade ESG data, Novisto is empowering more effective decisions and disclosures.

Navigate the transformation that’s underway with our CSRD Solution Overview.