In the quest to make corporate sustainability disclosures more easily accessible and comparable, digitization will become an invaluable ally. In particular, the ability for both machines and humans to find exactly the quantitative and qualitative data they’re looking for thanks to Inline XBRL reports may prove to be a game changer.

What is XBRL and what is it used for?

XBRL stands for eXtensible Business Reporting Language. First developed in 1998 for financial information, it is a set of specifications used for digital business reporting - reporting using machine-readable forms rather than traditional paper or electronic reports in PDF that are only readable by humans. In the private sector, XBRL has become the international standard for digital reporting of financial, performance, risk, and compliance information. It is also now becoming the mechanism to digitally tag many other types of disclosures.

Reports filed in XBRL format apply an XBRL taxonomy that defines a set of human and machine-readable terms or concepts that provide a digital representation of a set of disclosure rules. The taxonomy can then be used to markup a company’s reported data (facts) with these machine-readable terms in the XBRL language. This is done through XBRL tags, which indicate contextual information that describes the data to a machine, enabling it to find and “read” the data and its contextual information without human intervention. XBRL tags can be applied to both numerical data and blocks of narrative text, both long and short. The contextual information about the data, often called metadata, includes the fact’s time period, source, date, unit, change from previous year, and more. For example, a report by company X may state that it had revenues of US$90,000,000 in 2022. In the XBRL language, it would look like this:

- fact value = 90,000,000

- concept = revenue

- entity = company X;

- unit = USD

- time period = 1 Jan 2022 to 31 Dec 2022

To be able to apply XBRL tags to information in a report, the latter must be produced in certain formats. These include XML, HTML, JSON, and CSV.

XBRL taxonomies

An XBRL taxonomy links and defines a number of taxonomy components that provide the contextual information for facts in an XBRL report. For example, a taxonomy for an accounting standard would include definitions of concepts such as "profit", "revenues", and "assets". Taxonomies typically contain links (known as references) to authoritative definitions coming from accounting standards or regulations, as well as validation rules, calculations, and other relationships.

XBRL taxonomies are developed by standard setters, financial or otherwise, and companies reporting under one of these standards apply the standard’s taxonomy in filing XBRL reports. In the case of financial disclosures, for example, there are taxonomies for the US GAAP as well as the IFRS financial reporting standards. While XBRL is not a reporting standard per se, it’s interesting to note that the use of XBRL tags both depends on the existence of standards and facilitates their implementation.

XBRL or iXBRL?

iXBRL stands for Inline XBRL, an open standard that enables XBRL tags to be embedded in an HTML document that can be viewed by a human in a regular web browser. In other words, while XBRL filings are produced in XML format and are only machine-readable, iXBRL filings produced in HTML format are both human- and machine-readable.

In a standard web browser, an iXBRL report looks like a regular report. However, machine readers can recognize and extract the information that is tagged, along with its contextual information. A human reader can use a web-based review and consumption software (called a “viewer”) to also recognize the information that is tagged and see its contextual information. There are several such viewers available, many of them free to use. XBRL International has a published list of XBRL Certified Software (including applications to validate, create, and view XBRL tags) that has been inspected and certified for conformity with XBRL specifications.

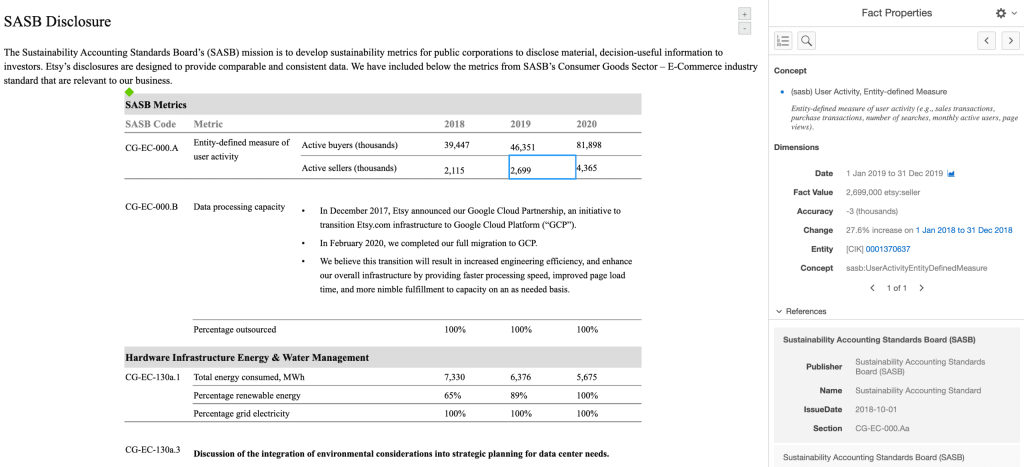

Sample iXBRL report seen with iXBRL “viewer” software

Source: Etsy (link)

XBRL International recommends using iXBRL for open reporting requirements, where the report preparer has control over the content of the report and how it is presented and there is a need to make the report accessible to both humans and machines. It recommends using XBRL for closed reporting requirements, where content and presentation are prescribed by the collector (for example through a pre-filled form) and where there is no need to make the report accessible to humans.

XBRL and iXBRL in sustainability reporting

In recent years, key actors in the ESG or sustainability reporting space have been moving towards adopting XBRL for sustainability reporting. No doubt one of the drivers for this is the convergence and alignment of sustainability reporting with financial disclosures, for which XBRL tagging is already common practice.

In September 2021, the Sustainability Accounting Standards Board (SASB) released an XBRL taxonomy for its 77 industry-specific disclosure standards. In a recent pilot project conducted by XBRL US, Moody’s Corporation and Etsy, Inc. produced iXBRL reports using the SASB XBRL taxonomy to illustrate that companies can leverage XBRL tagging to improve the availability, timeliness, and quality of their reported ESG data.

In May 2022, the International Financial Reporting Standards (IFRS) issued a staff request for feedback to inform a proposed IFRS Sustainability Disclosure Taxonomy for the upcoming IFRS Sustainability Disclosure Standards. This taxonomy is expected to be published for public consultation by the end of 2022 and to be finalized in 2023.

Also in May 2022, the European Financial Reporting Advisory Group (EFRAG) published a limited first draft of an XBRL taxonomy for the European Sustainability Reporting Standards, for the draft ESRS E1 standard on climate change.

XBRL and iXBRL in regulations

Today, XBRL tagging of financial information is mandated in several jurisdictions across the world. It is used by more than 100 regulators in over 60 countries including Japan, the US, and the EU. Companies in these jurisdictions follow the XBRL taxonomy prescribed by the local regulatory authority (US GAAP, China’s Securities Regulatory Commission, IFRS, etc.). In other jurisdictions such as Canada, South Africa, and Saudi Arabia, XBRL tagging remains voluntary. In a recent study, CPA Australia found that uptake by reporting issuers was significantly lower in jurisdictions where tagging remains voluntary.

Mandatory XBRL or iXBRL reporting by G20 country

| G20 country | Capital market/registrar mandate |

| Argentina | N/A - no project |

| Australia | Voluntary |

| Brazil | N/A - no project |

| Canada | Voluntary |

| China | Mandated |

| France | Mandated |

| Germany | Mandated |

| India | Mandated |

| Indonesia | Mandated |

| Italy | Mandated |

| Japan | Mandated |

| South Korea | Mandated |

| Mexico | Mandated |

| Russia | N/A - no project |

| Saudi Arabia | Mandated |

| South Africa | Mandated |

| Turkey | Mandated |

| UK | Mandated |

| US | Mandated |

EU | Mandated |

Source: CPA Australia (link)

XBRL is gaining traction among regulators because it facilitates disseminating and analyzing large amounts of information. It also introduces a greater capacity for compliance monitoring and supervision across large-scale samples.

In March 2022, the US Securities and Exchange Commission (SEC) proposed new rules to enhance and standardize climate-related corporate disclosures, which include the requirement for companies to electronically tag both narrative and quantitative climate-related disclosures in iXBRL.

In June 2022, the European Commission came a step closer to finalizing the adoption of the Corporate Sustainability Reporting Directive (CSRD), which will require companies to tag their reported sustainability information according to the XBRL taxonomy developed by EFRAG mentioned above and to produce their report in XHTML format.

The future of sustainability reporting is digital – and tagged

By publishing reports with XBRL tags, companies have confidence that their reported data can be consumed and analyzed accurately by both machines and humans. Consumers of these reports can quickly access large quantities of data for analysis and:

- test reporting facts against a set of business, calculation, and logical rules to avoid mistakes in analyzing and using the data;

- use the reported information to best suit their needs, including using different languages, alternative currencies, and preferred styles;

- validate reported information against a standard’s requirements for such information.

In much the same way as they have been for financial disclosures, XBRL and iXBRL formats are quickly being adopted by standard setters and regulators for disclosures of sustainability and ESG information. And like everything else in the corporate sustainability reporting space, it’s happening fast.

This article is heavily based on information and resources from XBRL International. For a deeper dive on key terms and uses of XBRL and iXBRL reporting, see XBRL International’s XBRL Glossary.