The ESG information disconnect—between what investors are asking for and what companies are providing—has been well identified. The rapidly evolving landscape of sustainability reporting is testimony to the efforts deployed to try to address this disconnect. These efforts are thwarted by the equally rapidly evolving needs of stakeholders, especially investors and increasingly capital providers more broadly, for ESG data that is more quantitative, more granular, more material, and more decision-useful.

One of the reasons for the information disconnect is the fact that corporate sustainability reporting has traditionally existed apart from traditional reporting and disclosure functions. As a result, it has remained on the outside of the rigorous and well-established collection, validation, and accountability processes that have benefitted financial disclosures and reporting. Traditional corporate social responsibility documents might better be described as communicating, rather than reporting.

To be clear, communication is essential to all organizations, which must convey all kinds of information to many different stakeholders for different purposes. In the context of capital markets, communication is the “lifeblood” that ensures that capital is appropriately allocated: as intended, based on all relevant information and at the right price, or, more specifically, the right risk-return trade-off. In this context, information must be decision-useful, i.e. on issues that are material to the company, consistent over time, comparable among peers, balanced in tone and content, easily understandable, reliable because externally audited, and timely relative to the period reported on. This type of communication must be circumscribed and regimented, and it is called reporting.

It’s understandable, therefore, that growing demands for sustainability-related information are leading to calls for more and better reporting. One such example is the International Organization of Securities Commissions (IOSCO) recently stating that it “sees an urgent need to improve the consistency, comparability, and reliability of sustainability reporting”.

What makes reporting different?

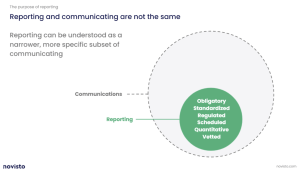

Reporting is a mechanism for accountability and an essential component of the planning–organizing–leading–controlling management process. It distinguishes itself from other forms of corporate communications by being:

- Obligatory: as a mechanism of accountability for commitments and actions

- Standardized more uniform, more consistent over time and between organizations

- Regulated: prescribed and reviewed by an independent authority

- Scheduled: recurring at specific intervals

- Quantitative: in nature, at least to some extent

- Vetted: internally and externally audited

Reporting can be understood as a narrower, more specific subset of communicating

Why does it matter?

The paradigm shift to the integration of sustainability that is currently sweeping both capital markets and the corporate world is certainly fueling the growing demand for more and better ESG information. But as we’ve just seen, not just any information, and not just randomly communicated. Indeed, to be widely available, information must be mandatory; to be comparable it must be standardized; and to be reliable it must be externally assured or audited. We would also add that, to make all of that easier, it must also be digitized.

This is exactly what we are seeing happening across the globe.

For instance, many are watching the European Commission closely, which earlier this year released its proposal amending the reporting requirements of its Non-Financial Reporting Directive under a new Corporate Sustainability Reporting Directive (CSRD). This new directive essentially mandates sustainability disclosures for both public and private companies, to be produced according to mandatory EU sustainability reporting standards (currently being developed), externally audited, prepared in XHTML format and tagged according to a digital categorization system that would be developed together with new sustainability reporting standards.

In the US, it has been difficult to keep up with the pace of change since the Biden Administration took office. There has been a slew of executive orders and public statements from high-profile senior officials, including the US Treasury Secretary and the Chair of the SEC, calling for mandatory and standardized climate-related and other ESG disclosures. The SEC has indicated its penchant for leading the creation of an effective ESG disclosure system and launched a public consultation on current climate change disclosures. On a smaller scale, but no less noteworthy, is California's Climate Corporate Accountability Act. Should it become law later this year, it would require all companies with more than one billion dollars in total revenues and doing business in California to provide audited reports of their GHG emissions by 2024, in accordance with a state-level climate reporting standard, and housed on a new digital platform.

Perhaps most significant, given its global reach, is the preparatory work of the International Financial Reporting Standards (IFRS) Foundation to establish an international sustainability reporting standards board. This has been very publicly and enthusiastically supported by IOSCO. By adopting a building blocks approach, IFRS expects to issue standards that provide a globally consistent and comparable sustainability reporting baseline, while also providing flexibility for coordination on reporting requirements that capture wider sustainability impacts. In its feedback statement on the consultation paper on sustainability reporting, IFRS Trustees have suggested it will be important for the new board to consider a digital strategy from the onset of its standard-setting, including the development of a taxonomy for the IFRS sustainability standards comparable to work being done on IFRS financial disclosures taxonomy.

But reporting is only for large public companies, right?

Given the attention lavished on all things ESG-related as of late, one might wonder whether all sustainability information should be regulated, standardized, audited, and digitized. Of course, this is neither desirable nor practical. As we mentioned, communication needs are broad and diverse, and so, too, should its channels. But it does stand to reason that these characteristics will remain important qualifiers to distinguish reporting from communications.

By the same token, one might also wonder whether sustainability reporting should apply not only to publicly listed companies, but also to private ones. And not only the largest companies, but small- and medium-sized ones as well. We believe this will likely be the case, for two main reasons. First, the demand for decision-useful sustainability information is coming from multiple stakeholders, not only investors who invest in all types of assets (not just public equities), but also large customers seeking to better manage their supply chains, lenders, insurers, consumers, and employees. Second, the greater scrutiny on sustainability-related issues is rooted in a more holistic, long-term, and forward-looking assessment of risks and opportunities that have direct consequences on a company’s operating and financial performance, risk profile, reputational capital, and prospects.

In other words, the scrutiny of sustainability reporting is intimately connected to enterprise value creation. This holds true for companies of all shapes and sizes—and there is no reason it should remain the privilege of only the largest companies.